Audit Fees are costs incurred by companies to pay public accounting firms to audit the company’s financial statements. There are many studies related to the association of audit fees with audit quality research including Asthaana and Boone (2012). Also the effect of audit fees on auditor independence has been carried out by previous researchers such as Barkess (1995), Supriyono (1988), Rusmanto (2002). In the study of Asthaana and Boone (2012) they found that abnormal audit fees (audit fees that are outside the norm / above average) are negatively related to audit quality issued by audit firms.

In research conducted by Supriyono (1988) audit fees are one of the factors that can influence auditor independence. Similar opinion is also supported by the findings of research conducted by Rusmanto (2002). Both Supriyono (1988) and Rusmanto (2002) studies were conducted in Indonesia. Whereas research does not support that audit fees do not affect auditor independence is a study conducted by Barkess (1995). So there are no conclusive results or agreement from the results of previous studies about the impact on the independence of audit fees or the quality of audit work.

In the daily life, audit fee some time become a challenge for auditor to show their independence in doing audit work. Because some people will arguing that the more audit fee recevide from the clients the less auditor become independent. This opinion must be clarified with audit work and professionalism of auditors.

Some researches findings have confirmed and some have confront the opinion spread in the public.

TR

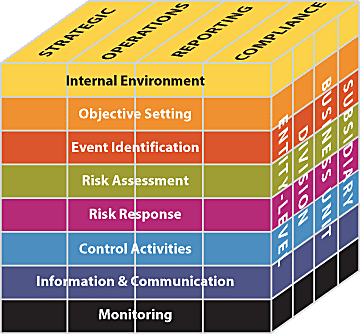

Image Source: Google Image

It okay for you